Inventory tracking and management isn’t as simple as entering a few item numbers in your inventory management software.

Jun 22, 2021 9 min readWe are committed to sharing unbiased reviews. Some of the links on our site are from our partners who compensate us. Read our editorial guidelines and advertising disclosure .

If you’re just starting an inventory system for your small business, it can feel overwhelming. What are all these terms and acronyms? Do you need inventory management software? And what is the best small-business inventory software, anyway?

We at Business.org are here to help. We’ve compiled a comprehensive inventory management guide to give you a solid understanding of inventory, a few pointers on how to manage your products, and a jumping off point for finding the right inventory tracking solution for your business’s needs.

So let’s get started.

That’s the million-dollar question, isn’t it? We’ve been doing comparisons on different software and chose Ordoro as our top option for its comprehensive features as a one-stop inventory management and dropshipping software solution. We’ve also got options if you have an ecommerce business or need warehouse inventory management software, plus budget picks for small businesses using online software .

At the end of the day, it’s going to depend on what features you need and the plan that works for your budget. We’ve done the work, looking at all the software options out there so you can choose which is best for your business.

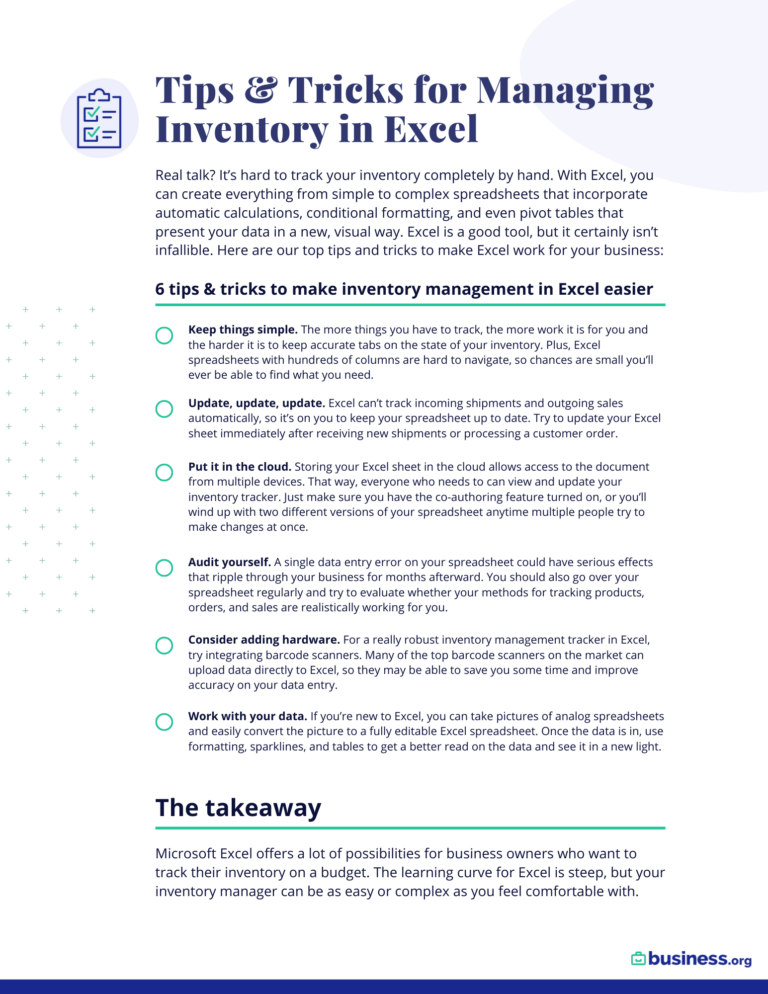

Keep your inventory organized, monitor shipments, and track vendor reliability with our customizable Excel inventory template and our included tips and tricks.

By signing up I agree to the Terms of Use and Privacy Policy.

Inventory is any type of physical assets owned by your business. Raw materials used for building or assembling products? That’s inventory. Products you’ve purchased from a vendor that are still working their way through your supply chain? Inventory. Items used to maintain your business (like cleaning supplies or computers)? Still inventory. And an inventory management system can help you keep tabs on it all.

Most often when people refer to inventory, though, they mean products that you intend to sell. That’s why most inventory management software is geared toward retailers and wholesalers.

To get more handy definitions to help you contextualize all the inventory tracker options available to you, check out our glossary of must-know inventory management terms and acronyms:

Technically, there are a lot more than four types of inventory, but we can fit most of it into these four categories

Part of effective inventory management is understanding the types of inventory you’re working with. For instance, if you frequently deal with work-in-process items, you may need inventory management software that offers supply chain management. Or if you have a lot of MRO items (like computers, for example), you’ll need a solution with asset tracking included.

To find out more about the types of inventory and get help with managing specific inventory types, check out the following guides:

Of course, just as there are different kinds of inventory, there are various theories on how to prioritize the items you reorder.

Maintaining good inventory management for your business means you have to stay on top of inventory turnover and ensure that you have enough finished goods to meet product demand. But there are other ways. These are the three major inventory management techniques:

Each of them has their own advantages and disadvantages, and it will depend on your inventory turnover and supply chain to see what is feasible for your business.

In the meantime, check these guides out as a way to figure out what your business needs:

Every business is different, but no matter what, you want to keep focusing your inventory management process on two things:

If you can maintain your stock level to meet customer demand, then your business will be successful. Inventory management software will take away the guesswork. What you need to do is determine which of the three major inventory management techniques you'll use and then how to implement that into your product purchasing and selling.

We’ve found four simple steps that can help businesses manage their inventory the best:

With the right inventory management process, you can be on your way to prioritizing the customer and staying ahead of the competition, while ensuring your business has the right tools to succeed.

Check out some of our top picks for inventory management software this year.

Part of what makes inventory management so complex is the sheer number of theories on the best way to track, reorder, and quantify inventory.

With ecommerce growing as a marketplace for businesses—and global shipping becoming equally important—finding an inventory management system that extends your business’s reach is just as important as software that makes the job easier. Although there are numerous ways to track inventory, the best software will home in on the features you need without bogging you down in useless extras.

Every business is different, so we recommend getting started with our overview of what inventory management is (and how it can help your business). From there, you can see what you need—ecommerce options, a QuickBooks integration, or warehouse management —and use our reviews as a guide.

One of the big concerns inventory management tries to address is the best way to reorder products. You want to make sure your inventory levels stay high enough to meet customer demand, but you also don’t want to wind up with excess inventory that won’t sell (and the potentially high inventory costs associated with storing those items).

To find out how to balance your inventory needs with your cash flow, calculate your safety stock, and determine your reorder points for your products, check out our explanations of the most commonly used reordering methods:

Businesses also need to determine how they plan to track their inventory levels. There are two main schools of thought on the matter:

Periodic inventory tracking requires taking a physical count of your inventory periodically—at the end of the month, quarter, or year. This, of course, is not optimal for all businesses, and can make tracking your inventory more difficult. Meanwhile, perpetual inventory tracking is focused on cost and stock levels on a transaction-by-transaction basis, allowing your business to continually update what's available, the cost, and your bottom line.

Some businesses need constant updating while others can wait. This guide should help you decide which option works better for you:

Another main component of inventory management? Costing. Costing helps you balance the books and calculate important metrics like your profit margins and your cost of goods sold (see our inventory glossary to learn more about that). Here are a couple of resources to help you decide how you allocate costs:

If you choose to use the first in, first out method ( FIFI Method) , you’ll be focused on selling the oldest items in your inventory first. That’s because the oldest cost (i.e. purchase order) for goods is going to be applied to the first batch of sold goods. If you sell the oldest goods first, you’ll be paying off the oldest purchase order (for those goods) first.

On the other hand, the last in, first out method ( LIFO Method) applies the cost of the most recently ordered items to the most recently sold goods. Although it’s not commonly used outside of the US, the method does provide your business with a major tax advantage (by focusing on new costs first) and allows you to focus on the most current financial numbers while providing a great customer experience by selling the most recent products first.